Bond markets have for years been seemingly close to a tipping point when it comes to electronic trading, yet they could never quite breakthrough. Yet those who closely follow technological advances and market structure were unwavering. “The slow and steady change that has occurred over the past decade will ultimately be seen for the revolution that it brought about,” Kevin McPartland, head of research in Greenwich Associates’ market structure and technology group, wrote in a January 2020 report.

Source: Bloomberg

That belief — that fixed-income trading wasn’t entirely impervious or antithetical to progress — has finally paid off, even if it took a global pandemic to get there. No matter how you slice it, the momentum toward automation, electronic trading and consolidation in a once-fragmented space is undeniable.

At the highest level, MarketAxess Holdings Inc. and Tradeweb Markets Inc., two of the dominant companies in the bond-trading industry, each reported their highest yearly trading volumes on record in 2020. That hasn’t let up, either: Tradeweb, known primarily for its U.S. rates marketplace, said last week that average daily trading volume in January was $1 trillion, while credit trading at MarketAxess was $12.4 billion a day. Both of those figures exceed the levels reached in March 2020, which was most volatile month for financial markets during the Covid-19 pandemic.

The trend extends beyond just dollar volumes, though. These entrenched players are cementing their place in the global fixed-income markets with strategic acquisitions and advancements that make bond trading more streamlined. In one of the more notable moves, Tradeweb agreed earlier this month to pay $190 million in cash to acquire Nasdaq Inc.’s fixed-income trading platform, originally known as eSpeed. Bloomberg News’s Elizabeth Stanton and Liz Capo McCormick provided great historical context about the combined entity:

The deal unites two businesses that in the 1990s helped invent electronic trading of U.S. government debt. Tradeweb was launched in 1998 as the first electronic platform connecting dealers with institutional investors in Treasuries. ESpeed’s instant success after its 1996 debut so unnerved bond dealers that they launched their own platform, BrokerTec, in 1999.

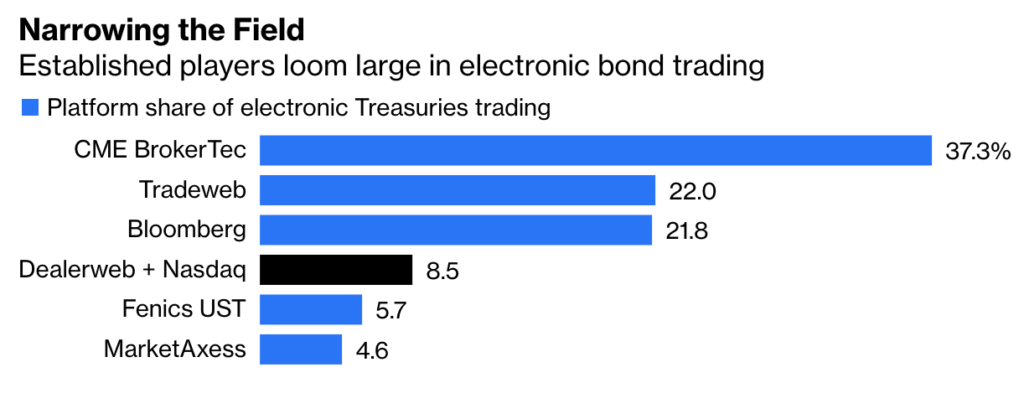

BrokerTec had about 60% market share and eSpeed 40% of interdealer electronic trading of Treasuries when Nasdaq bought eSpeed from Cantor Fitzgerald LP affiliate BGC. But as of this past December, the renamed Nasdaq Fixed Income’s average daily volume in Treasuries was $13 billion compared with $86 billion for BrokerTec.

Tradeweb, by combining the Nasdaq market with its interdealer trading business called Dealerweb, will have over 20% market share of wholesale electronic trading of Treasuries, making it competitive with BrokerTec and Fenics, McPartland said.

For those who aren’t steeped in the inner workings of the $21 trillion U.S. Treasury market, reading this could make your head spin. The success of eSpeed, which will be combined with Tradeweb’s Dealerweb, led to the rise of BrokerTec, which, by the way, as of last week completed the migration of its Treasuries trading and U.S. repo platform to CME Globex. Then eSpeed was sold to Nasdaq by BGC and Cantor, which turned around and created Fenics. Got all that?

Narrowing the Field

The jargon also makes it difficult for those on the outside to get a sense of what is possible on these platforms. “Tradeweb will facilitate trading in U.S. Treasuries through direct streams, CLOB, request-for-quote (RFQ), sessions-based trading, automated trading, list trading and click-to-trade to clients in the institutional, wholesale and retail sectors,” it said in its statement announcing the acquisition. (CLOB stands for central limit order book.)

McPartland at Greenwich Associates put it this way in an interview: “In the end, it does seem that what traders like is to have choice in terms of how they execute and how they find liquidity, but they prefer to have a lot of that choice within one or two platforms, not five or six.” That might help explain why, for instance, OpenDoor Securities ceased operations earlier this year. Its pitch was a unique auction platform for directly connecting buyers and sellers of Treasuries.

That kind of niche strategy is different from the likes of Tradeweb and MarketAxess, which appear to be bulking up to serve just about any need of traders in Treasuries and corporate bonds. MarketAxess acquired LiquidityEdge, an electronic Treasuries marketplace, in August 2019 for $150 million. Then in December, it launched “a centralized fixed income trading marketplace that fully integrates rates trading capabilities within the MarketAxess trading system.”

Soon thereafter, Tradeweb launched “multi-client net spotting,” which is meant to help credit traders more easily access the Treasury market to hedge risk within the same platform. It replaces “the cumbersome process of manually spotting spread trades with one that enables hundreds of billions of credit trading flow to be hedged electronically,” Tradeweb said in its statement.

“It’s reached a point where there is broad acceptance that this is a sizable part of the market that isn’t going anywhere,” McPartland said of electronic trading. “We have a handful of big solid incumbents that have particular areas of strength. To some extent, each of them is trying to eat the others’ lunch, which is good and healthy competition to keep everybody on their toes.” (Bloomberg LP competes to offer fixed-income trading services, data and information to the financial industry.)

A Tipping Point?

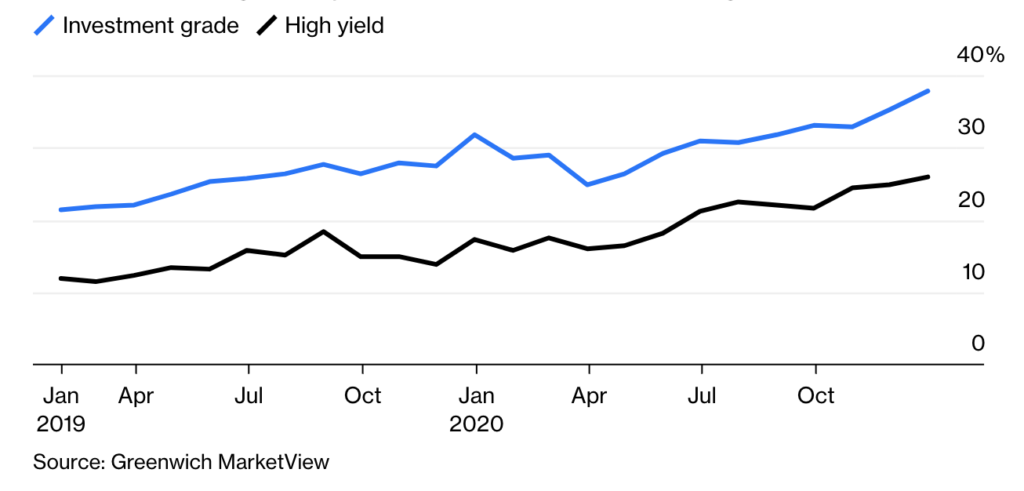

Electronic trading of corporate bonds soared to new heights in 2020

For all the electronic evolution, the bond market will probably never quite look like equities. Some trades are simply too complex, or involve securities that have little liquidity, that it will take some personal negotiation. But there’s growing evidence of creative workarounds, most notably the rise of portfolio trading, which allows credit traders to quickly buy and sell baskets of securities using the create-redeem function of exchange-traded funds. It’s such a lucrative business, in fact, that Goldman Sachs Group Inc. has asked some traders in its portfolio-trading group to sign a six-month noncompete clause to get their 2020 bonuses, Bloomberg’s Sridhar Natarajan and Lananh Nguyen reported.

Goldman struck a deal in October with MarketAxess in which it committed to become a dedicated market-maker and contribute streaming prices for U.S. investment-grade corporate bonds. The MarketAxess Live Markets order book “gives institutional credit investors and dealers the ability to place resting live orders in the market and engage firm prices provided by dealers and investors with a single click.” In other words, no need to call Goldman every time — just click.

Having Wall Street’s support, instead of long-held opposition, could be the last step to a fixed-income revolution. “It’s almost gone full circle, and now the most sophisticated dealers have learned how to operate very effectively in those electronic markets as well,” McPartland said.

I remember in September 2019, during a conference held at the Federal Reserve Bank of New York, when Scott Minerd at Guggenheim Partners lamented the “archaic method” of calling three dealers to obtain a bond price. “It’s a low-value add. We’re not curing cancer, we’re getting a quote on a bond,” he said.