Discerning investors could eke more gains out of developing-nation bonds, but the bulk of the rally in the riskiest corners of the market may have passed.

Source: Bloomberg

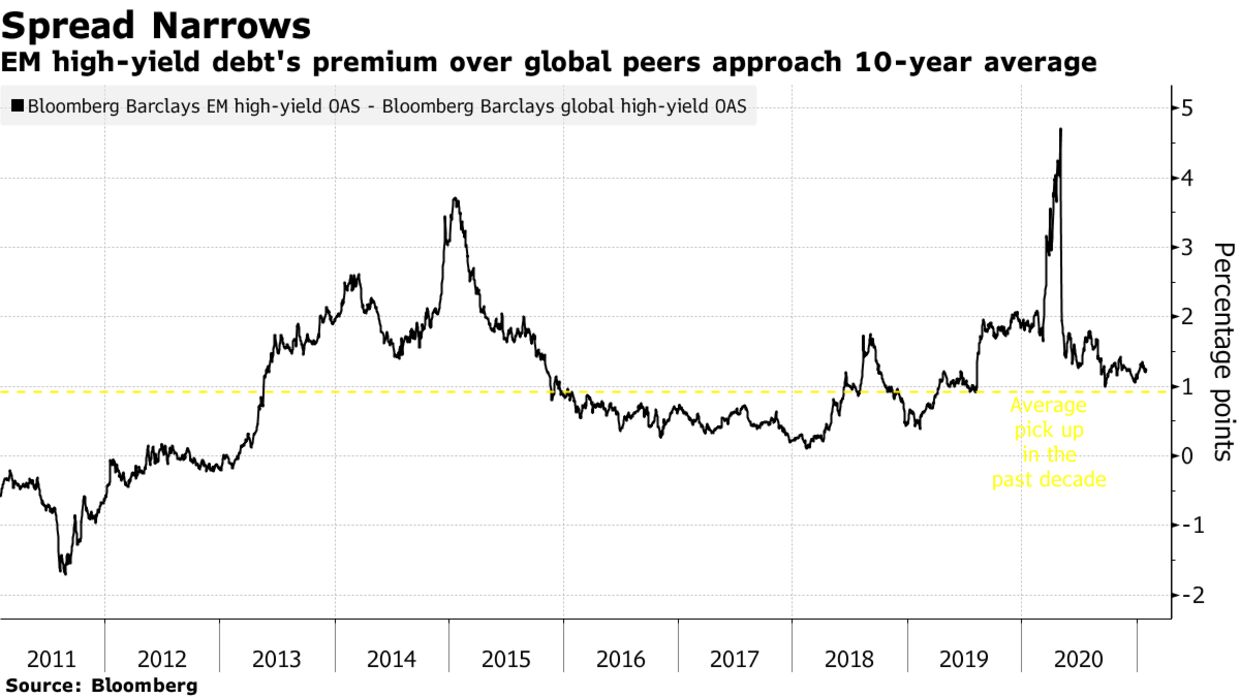

The gap between spreads on emerging-market high-yield debt and global peers has narrowed from a record 470 basis points in May to 127 basis points, close to the 10-year average of 94. Developing-nation high-yield bonds lost 1% in January, halting a two-month rally that handed investors returns of more than 8%.

Morgan Stanley prefers debt rated BB and stronger single B, urging investors to differentiate between credits by assessing borrowers’ external funding vulnerabilities and prospects for reforms as the coronavirus pandemic pressures economies. With oil prices rebounding, Fidelity International favors energy-linked borrowers such as Oman and Mexican oil producer Pemex.

“There is some value in selective BB rated names in emerging markets, but most of the spread compression and total return gains have already come and gone,” said Paul Greer, a London-based money manager at Fidelity International, whose debt fund outperformed 90% of peers in the past three years.

“We have much less conviction on B or CCC-rated emerging-market credits with elevated cash prices,” he said. These include Costa Rica, El Salvador and Angola, which were among the biggest gainers in January.

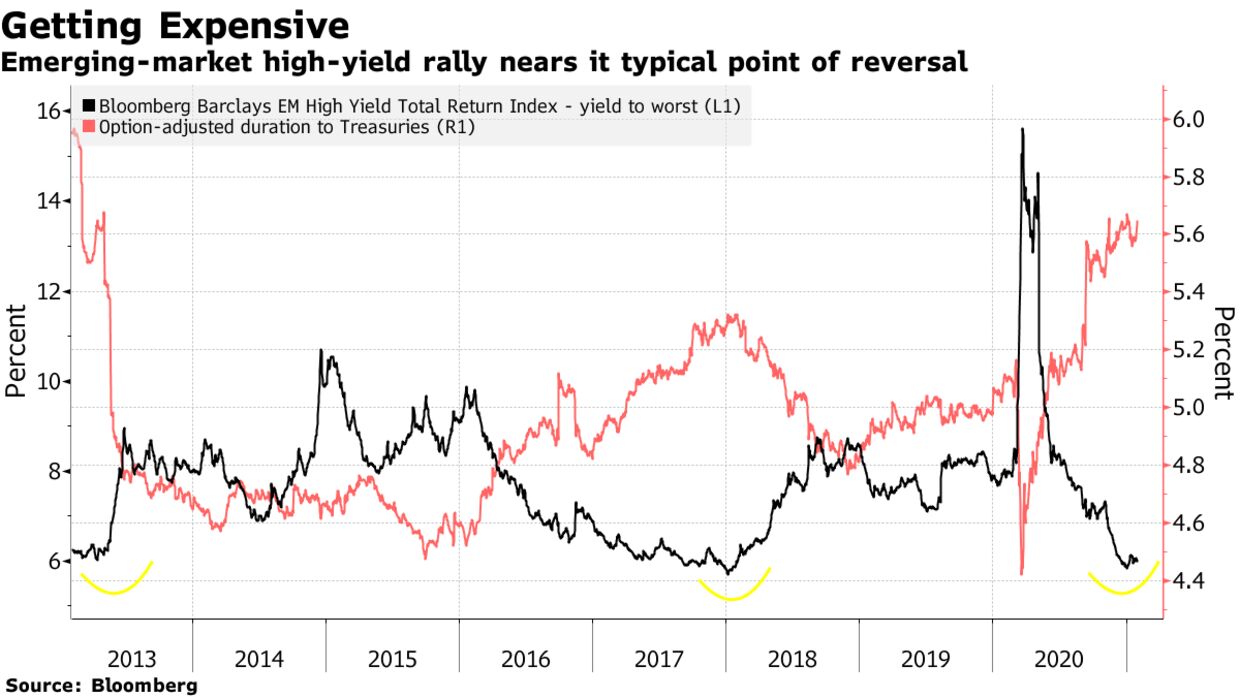

There are other signs that the rally has matured. High-yield bonds in emerging markets have become the least remunerative to investors, and the riskiest, since May 2013, based on the option-adjusted duration on the Bloomberg Barclays gauge for the debt. This measure of sensitivity to interest-rate changes has risen to 5.65%.

The last time it was that high, eight years ago, the index’s yield rose 3 percentage points in as many months. The yield itself has fallen to its 2018 low, evoking memories of the selloff fueled by the U.S.-China trade war.

A surge in U.S. yields will probably cause sentiment toward riskier assets to sour. While that is likely to happen in the event that the Federal Reserve pulls back its asset purchases or there’s a faster-than-expected rise in inflation, that’s at least “several quarters away,” said Bryan Carter, global head of emerging-market debt at HSBC Global Asset Management in London.

“Although high-yield credit spreads are back to historical average levels, having recovered from the Covid-19 crisis panic period, we see room for spreads to enter a euphoric zone based on a Goldilocks combination of economic growth rebound, easy monetary policy and another fiscal stimulus from Congress,” Carter said. “This could last several months or quarters.”

Even then, the manager prefers credits from Africa and in the Middle East that have been “mispriced” by expectations of new supply or the lack of recent market access, while avoiding sovereigns with debt-sustainability issues or untenable debt service levels.

Tidal Wave

What’s moving marketsStart your day with the 5 Things newsletter.EmailBloomberg may send me offers and promotions.Sign UpBy submitting my information, I agree to the Privacy Policy and Terms of Service.

A tidal wave of monetary support and optimism that coronavirus vaccine rollouts will sustain a global economic recovery, amid more than $16 trillion of negative-yielding debt worldwide, have emboldened investors to hunt for returns in riskier assets. That enabled junk-rated sovereigns, including Turkey, Oman and Benin, to cushion the blow to their budgets from the pandemic by selling bonds last month that yield as high as 7.25%.

“That’s been giving investors comfort that the market is open and there’s time for countries to appropriately adjust policy,” said Michael Cirami, a Boston-based money manager at Eaton Vance Corp., which oversees $583 billion. But “there’s always a concern about a liquidity event turning into a solvency event,” he said.

Still, the riskiest of the risky has struggled to borrow. Laos, which was downgraded to CCC by Fitch Ratings in September, has yet to pull off a deal after last month reviving a bond offering that it had postponed in December.