Traditionally issued by high-growth companies, these securities have drawn tourism and travel companies who need to raise cash

Source: WSJ

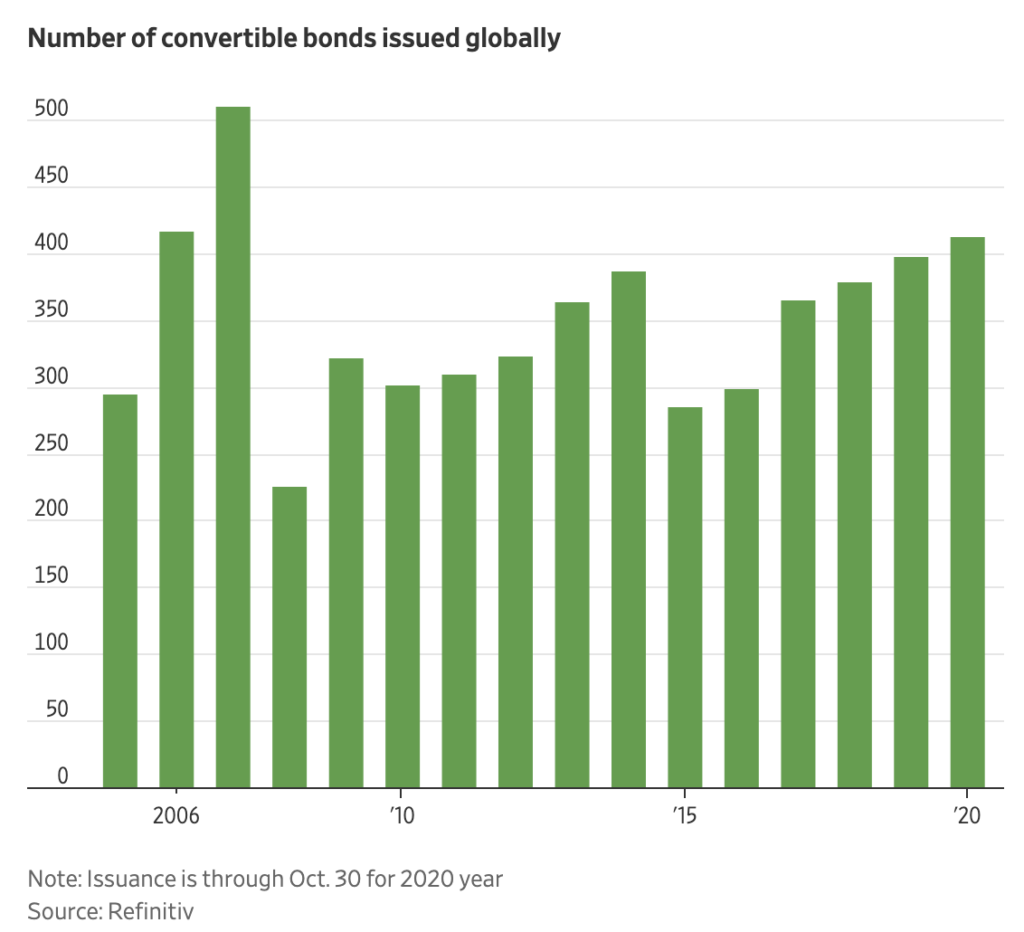

Companies hit hard by the coronavirus pandemic flooded the market this year with the most convertible bonds since 2007. Investors who scooped up these securities have been rewarded with strong returns.

Travel and hospitality companies including Carnival Corp., Southwest Airlines Co. and Royal Caribbean Group raised $147 billion through Oct. 30 globally from the sale of bonds that can be exchanged for stocks, using them as a cheap way to stay afloat through the pandemic. That compared with issuance of only $108 billion of such bonds by the same point in 2019.

Almost a third of the roughly $450 billion convertible bonds outstanding were issued this year. Companies began stepping up the pace of such sales in April, following a tumultuous month that saw investors pull money out of even the safest assets. Travel, tourism and hospitality companies, whose stocks were among the most beaten up, turned to these securities in the months through June.

Convertible bonds are a hybrid between a bond and a stock. Like bonds, they have a coupon that pays a set interest rate for a period, providing a steady return. But unlike a bond, if the company’s stock price rises above a certain threshold, the holder can convert the bond to stock, scooping up a tidy profit.

The interest rates that companies need to pay on convertible bonds tend to be lower than on regular bonds, since the investor gets a chance to profit if the share price rises. That has made them attractive for companies that became strapped for cash as the pandemic halted flights and cruises and closed shops and restaurants.

“In hindsight, the best way to play the [convertibles] market was to buy everything that came out because of the stock market’s V-shape recovery,” said Maxime Perrin, client portfolio manager at Lombard Odier Investment Management.

Convertible bonds in the Reuters Qualified Global Convertible Index are up almost 22% this year.

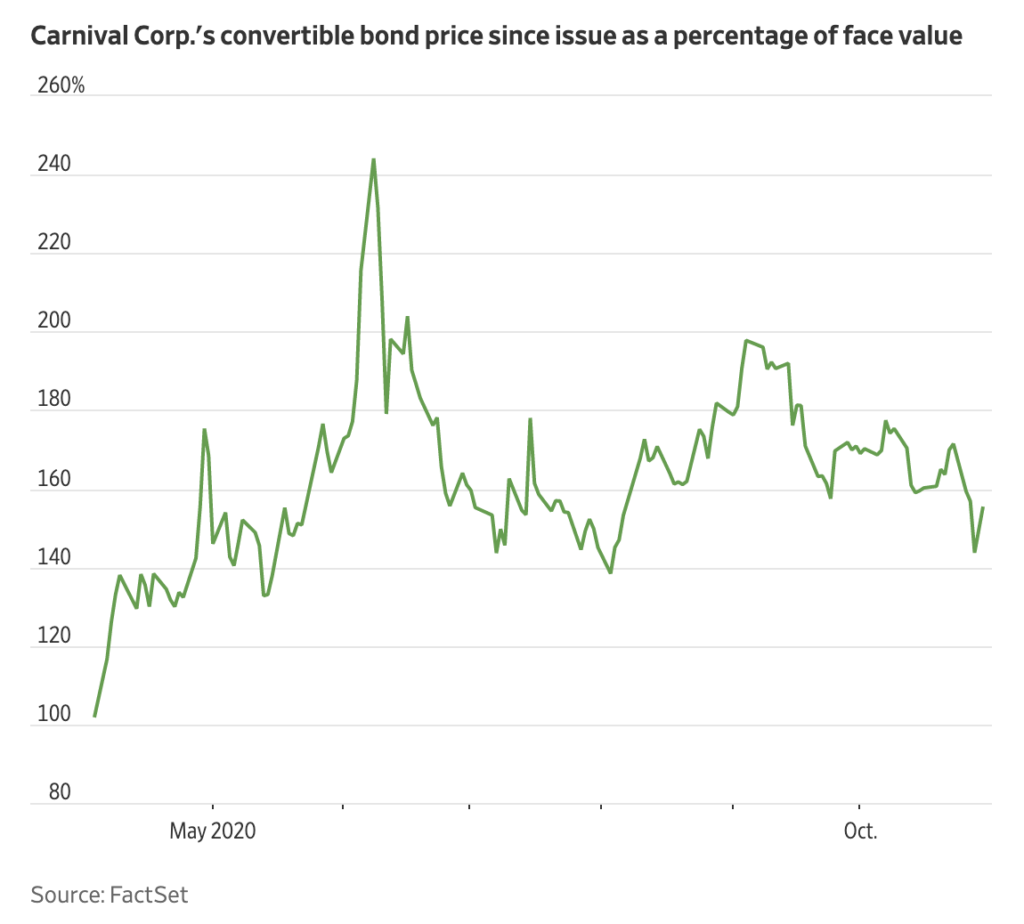

A $2 billion convertible bond issued by Carnival in early April with a 5.75% coupon now trades at more than 155% of its face value, according to FactSet, after shares in the cruise-line operator rebounded strongly from their lows. In the same month, Carnival issued $4 billion of regular corporate bonds with a coupon of 11.5%, twice the cost of the convertible.

The terms of Carnival’s convertible-bond sale gave investors the option to swap each security for 100 shares at $10 apiece, at a time when the stock was trading near its lowest this year. Four months later, after the stock price approached $15, Carnival redeemed nearly $900 million of these bonds early by offering investors 112 shares priced at $14.02 apiece for each note, which have a $1,000 face value.

That allowed holders of the convertible notes to book some profits, even if it meant giving up on some of the potential upside.

Hedge funds and investment bank’s proprietary-trading desks used to dominate the market. They would buy convertible bonds, then trade the equity and credit risks linked with them separately, often using derivatives and leverage to exploit small differences in values.

Nowadays, longer-term buy-and-hold investors have become more important. Investment bank proprietary-trading desks are gone and leverage for risky trades is much harder to get for hedge funds.

Mr. Perrin is a long-term holder looking for deals that will do well over many years, rather than a short-term trader or arbitrage specialist hunting for quick profits. That means this year he has missed out on some sharp, quick returns, but he isn’t convinced all the deals will still look as attractive in a few years.

“I don’t think cruise companies are out of the woods,” Mr. Perrin said. “I don’t see bookings picking up substantially.”

He has favored companies like Southwest Airlines, French aerospace group Safran SA, and Booking.com, BKNG -1.13% a younger, higher-growth tourism company.

“The issuance has been enormous, historic in nature,” said Kevin Russell, chief investment officer at UBS’s hedge-fund unit, O’Connor. “We saw this rush of issuance, and we ramped up our exposure to take advantage of that.”

Mr. Russell said he put some spare cash into the market and wound down some junk-bond exposure to add more convertibles. He has sold some positions lately to cement gains, but is optimistic for further strong performance as markets remain volatile.

Volatility is important because it directly influences the likelihood that a bond will convert into shares when it matures. This works exactly like stock options do: Higher volatility makes the conversion option more valuable because it improves the chances that the shares will rise above the price at which the bond can be converted into stocks.